Our Industry

Since the early days of the pioneers, the timber and forest products industry in New South Wales has been central to the economic and social viability of many regional communities across the state.

From Eden to Kyogle, Barham and Baradine there are nearly 22 million hectares of native forests in New South Wales and nearly 400,000 hectares of plantations. Below we distinguish between hardwoods and softwoods and identify where they are grown and the timber products they provide.

The state-owned Forestry Corporation of NSW and private forest owners supply timber, providing log products under contract to sawmills throughout New South Wales.

For generations, the timber industry has worked with the NSW government to harvest a small percentage of this natural resource to meet the state’s demand for unique forest products. The industry is a major employer in rural and regional New South Wales, employing 22,000 people and supporting many regional communities.

In fact, New South Wales’ timber and forest products industry contributes millions each year to the state’s economy. Below, we provide an introduction to each stage of the industry’s value chain, from forest management to primary and secondary timber processing.

The industry underpins vitally important supply and demand relationships with the Australian manufacturing, construction and property sectors. To understand recent developments, we provide details of supply and demand of timber in New South Wales below.

Download the Timber New South Wales Industry Brochure

Hardwoods & Softwoods

In New South Wales there are 63 hardwood mills and 13 softwood mills processing more than 5.6 million cubic metres of sawlogs every year.

Hardwoods

Almost all native timbers harvested in NSW are from hardwood species (eucalypts) which grow in tall native forests along the coast and tableland. In total there are over 50 commercial species, the most common being Coastal Blackbutt, Spotted Gum, Sydney Blue Gum, Stringybark, Silvertop Ash and Ironbark (refer Figure 1).

Figure 1 – Native forest, Sydney Blue Gum and Spotted Gum

Species such as Coastal Blackbutt, Spotted Gum, Flooded Gum, Dunn’s White Gum and Gympie Messmate are also grown in hardwood plantations located on the State’s north coast.

Hardwood forests provide timber that is visually attractive, dense, strong and durable. Hardwood timber is used for flooring, decks and pergolas (‘dry appearance timber’), for structural purposes such as power poles, wharves and bridges (‘green structural timber’) and for lower value applications such as landscaping sleepers, fencing and pallets (‘green other’).

Decorative hardwood furnishings account for small volumes but service high value niche markets. Timber unsuitable for use in solid wood products is sold as pulpwood for woodchip export or as firewood for domestic heating.

Softwoods

NSW produces one third of Australia’s softwood timber, most of it via plantations using exotic species such as Radiata Pine. Cypress Pine is a common native softwood species that is harvested from dry native forests located west of the Dividing Range.

Figure 2 – Cypress Forest

However, most softwood timber is grown in plantations using exotic species. The most common species grown are Radiata Pine and various Southern Pines, the dominant species being a hybrid of Slash Pine and Caribbean Pine.

Radiata Pine prefers a temperate climate and is grown in large scale plantations on the south-west slopes around Tumut, on the southern tablelands around Bombala and on the central west slopes around Bathurst-Oberon (refer Figure 2).

Smaller plantation estates are located near Braidwood, Moss Vale, Walcha and Inverell. Southern Pine is better suited to a subtropical climate and is grown on the far north coast, mainly around Casino and Grafton.

Exotic softwoods provide a light coloured, soft timber ideally suited for house frames and lower grade furniture (‘dry structural timber’). When treated, they are commonly used in outdoor applications such as decks, pergolas, landscaping and fencing applications. Low quality softwood logs and sawmill residues are used to make newsprint and cardboard, fibreboard, particleboard and reconstituted wood panels.

The Value Chain

The industry’s value chain begins with forest management and the sustainable production of native and plantation timber, continues with harvest and haul and ends with the primary and secondary processing of a wide range of wood products (refer Figures 3-6).

Figure 3 – Mechanical Timber Harvesting, hardwood, pine softwood

Figure 4 – Pine sawlogs being unloaded

Figure 5 – Loading a truck with hardwood pulpwood thinnings

Figure 6 – Transporting logs, hardwood, pine softwood

![]()

![]()

The New South Wales wood processing industry is diverse, with mills of all types and sizes spread across the state producing a wide range of wood products. In total there are 63 hardwood mills and 13 softwood mills processing more than 3.3 million cubic metres of sawlogs every year.

In primary processing, or milling, the raw log can be processed in six different ways. It may be retained in round form, sawn, peeled or sliced, split, chipped or crushed (refer Figure 7).

Figure 7 – Types of primary processing

Mill logs

Roundwood poles

Sawnwood

Peeled Veneer

Split Firewood

Woodchips

Sawdust Residue

Due to the natural variability in timber, the industry constantly strives to optimise the value of the products recovered from each processed log. The industry is careful to minimise waste and closely manages the production of lower value products, which can constitute a large proportion of the market by volume.

Hardwood round timber may be sold as high value, structural products such as poles, piles and bridge girders. However, sawlogs and sawn timber production is the mainstay of the industry and generates the greatest value for both the forest grower and the primary processor. The manufacturing process depends on the quality of the sawlogs.

High value veneer is produced by slicing or peeling logs and has a variety of value added uses (see secondary processing). Medium and lower quality logs may be cut and split into fence posts and firewood. Low quality logs known as pulpwood are chipped. The lowest value product is sawdust and this is sold to the equine, chicken and landscaping industries or burnt onsite to produce heat and energy.

Woodchips are also a by-product of sawn timber processing and can be used in landscaping. The greatest demand for woodchips however is in secondary processing where there are a large variety of applications (see below).

Sawn timber may be sold green or as a dried and dressed product. Most softwood sawn timber and over one third of all hardwood sawn timber is dried or ‘seasoned’ before it is sold. Drying timber makes it more stable and increases its strength and immunity to decay.

From its ‘green’ or unseasoned state, timber can be allowed to dry naturally (known as air drying) or dried in kilns. Kilns extract moisture by artificially controlling the drying environment, including the wind speed, temperature and humidity.

The mix of sawn timber products produced by NSW sawmills is detailed at Figure 8.

Figure 8 – Sawn timber product mix from NSW Sawmills by species group

Data source: ABARES (2013) Australian Forests and Wood Products Statistics

Secondary processing adds further value to timber through a broad range of manufacturing processes (refer Figure 9). Most secondary processing activities use lower value chipped fibre to produce commodity products like pulp and paper, cardboard, reconstituted products like fibreboard and engineered wood products like laminated veneer lumber.

These processors are typically large-scale, capital intensive manufacturing operations employing many people. Medium scale secondary processing operations tend to be associated with adding value to sawn timber products such as the production of softwood frames and trusses.

Secondary processing that produces higher value appearance products like hardwood furniture and joinery tend to be smaller scale and rely more heavily on the workmanship and skills of individual tradespeople.

Figure 9 – Secondary processing

Sawn Timber

Mouldings & Joinery

|

Frames & Trusses

|

Veneer Timber

Plywood & Formply

|

Engineered flooring and doors

|

Chipped Timber

|

Pulp, paper & cardboard |

Wood-based panels (Particle Board & MDF)

|

External Timber cladding

|

|

Round and Sawn Treated Timber

Wood treated with preservatives |

Demand & Supply For NSW Timber

Supply

In 2012–13 New South Wales accounted for 40 per cent of all hardwood sawlogs and 32 per cent of all softwood sawlogs processed and supplied within Australia.

The state-owned Forestry Corporation of NSW is the main supplier, providing more than 4.5 million cubic metres of log products annually to sawmills throughout New South Wales and beyond. The Forestry Corporation commissions more than 100 contractors to undertake harvesting and haulage operations on its behalf.

Hardwood

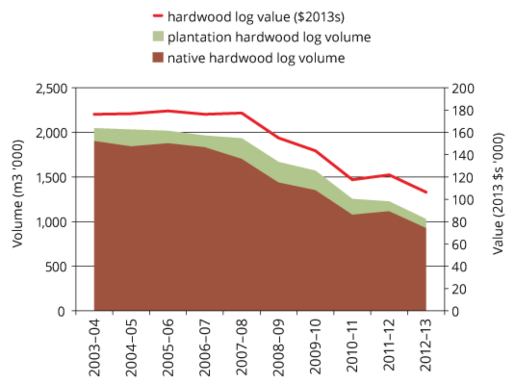

Over the last ten years hardwood log supplies in New South Wales have been reduced to accommodate new national parks and conservation reserves. The unit value of harvested hardwood logs has been maintained in real terms, however their overall value declined (in proportion with the reduction in supply) to $106 million in 2013 (refer Figure 10).

Figure 10 – Volume and Value of hardwood logs harvested from NSW forests by year (2003–04 to 2012–13)

Data source: ABARES (2013) Australian Forests and Wood Products Statistics

Softwood

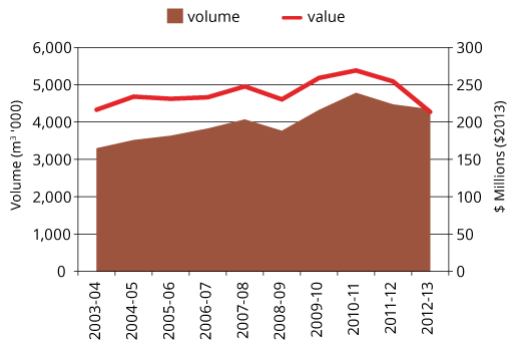

Supply of softwood logs from New South Wales forests has increased over the last ten years as many plantations reached commercial maturity. Over the same period, increasing global competition has reduced the unit price at which logs are sold. This has led to a slight reduction in the overall value of the resource to $214 million in 2013 (refer Figure 11).

Figure 11 – Volume and Value of softwood logs harvested from NSW forests by year (2003–04 to 2012–13)

Data source: ABARES (2013) Australian Forests and Wood Products Statistics

Demand

Domestic demand for NSW timber and forest products has remained solid over many generations. With a growing population and increasing need for building and construction products, the industry is well placed to meet demand for local timber products which are renewable, sustainable and support regional economies and jobs.

The timber and forest products industry in New South Wales is an important component of other industry sectors in Australia. In particular, the timber industry underpins vitally important supply and demand relationships with the Australian design, manufacturing, construction and property sectors.

- 75% of sawn timber produced is used in residential construction.

- 20% of timber consumed in Australia is used by the furniture industry.

- 5% of timber usage is by the kitchen sector alone.

International demand for New South Wales timber has begun to grow rapidly. In the 12 month period to December 2013, Australian roundwood exports increased 66 per cent by volume and 73 per cent by value to $73 million. Nearly all of this growth was attributed to increasing demand from China.

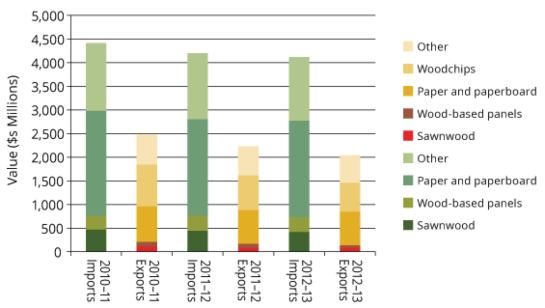

However, our export trade with China is relatively small compared with Chinese forest product imports into Australia. Doors, flooring and mouldings valued at $220 million were imported from China in 2013.

In the last decade Australia’s $2.1 billion trade deficit in wood products has remained relatively stable, with imports currently valued at $4.1 billion and exports value at $2 million (refer Figure 12).

Export demand for low quality products such as hardwood pulpwood (woodchips) has declined with a 42 per cent decrease in value over the last five years. This trend has beendriven by the high Australian dollar and strong competition from Vietnamese pulpwood resources. Paper and paperboard is now Australia’s most valuable wood product export.

Figure 12 – Value of wood products imported to and exported from Australia (excluding value added wood products)

Data source: ABARES (2013) Australian Forests and Wood Products Statistics